For businesses seeking fast, reliable funding, a business loan remains the most straightforward solution; it supplies the cash flow needed to expand operations, purchase inventory, or bridge seasonal gaps. Understanding the types, qualifications, and costs involved can turn a vague idea of borrowing into a concrete growth plan. In this guide we break down everything from SBA‑backed loans to unsecured working capital options, and we show how to match the right product to your company’s cash‑flow cycle – even if you’re just starting out. Learn how to choose the right small‑business loan.

What Exactly Is a Business Loan?

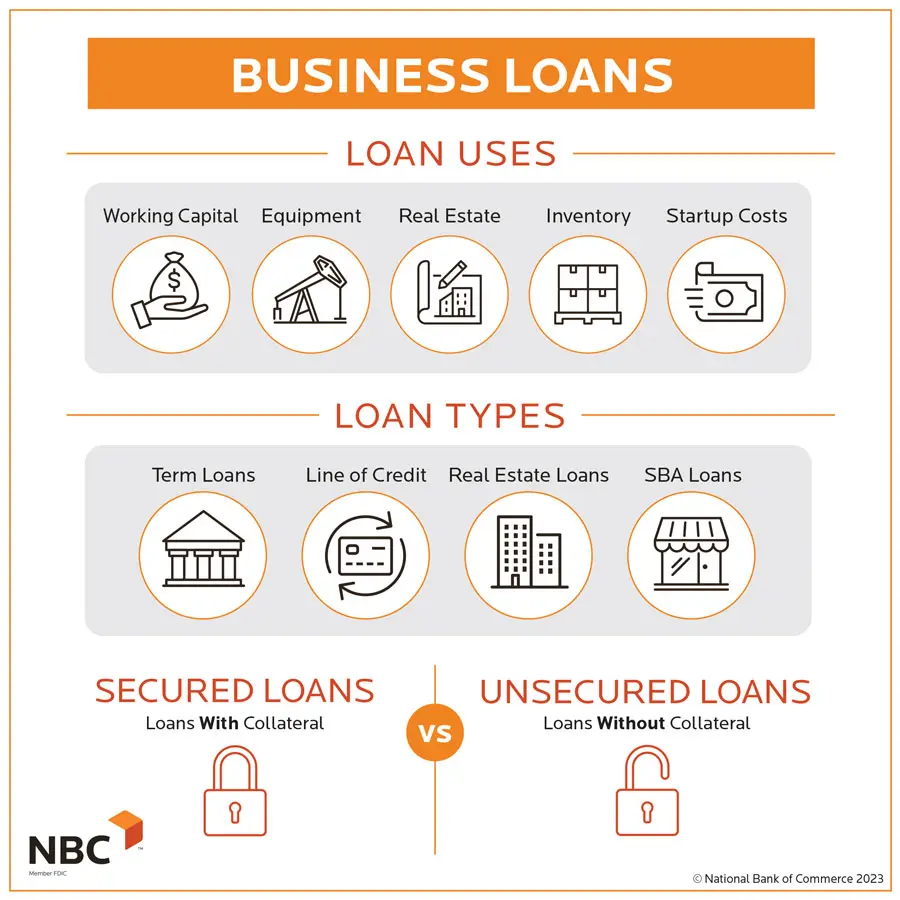

A business loan is a sum of money that a lender provides to a company, which the borrower repays with interest over a predetermined term. Unlike personal credit lines, business loans are evaluated based on the company’s creditworthiness, cash flow, and often the collateral offered. The most common categories include:

- Term loans – fixed‑amount, fixed‑rate financing repaid over 1‑10 years.

- Working capital loans – short‑term funds to cover day‑to‑day expenses.

- SBA loans – government‑guaranteed loans with competitive rates.

- Equipment financing – loans secured by the machinery or technology being purchased.

- Unsecured business loans – no collateral required, typically higher rates.

Why Companies Choose Business Loans Over Other Financing

According to the U.S. Small Business Administration 2025 report, 68 % of small‑business owners preferred traditional loans to alternative financing because of lower overall cost of capital and clearer repayment structures. Key advantages include:

- Predictable payments – Fixed monthly amounts simplify budgeting.

- Ownership retention – Unlike equity financing, you keep full control.

- Tax deductibility – Interest expenses are generally deductible, reducing net cost.

- Scalability – Larger loan amounts can fund multiple growth initiatives simultaneously.

Current Landscape (2025‑2026)

Data from the World Bank Global SME Finance Outlook 2026 shows that global business loan issuance grew 9 % YoY, reaching $1.3 trillion. In the United States, the average interest rate for a five‑year term loan fell to 5.2 % in Q1 2026, down from 6.1 % in 2024, reflecting tighter monetary policy easing and increased competition among community banks.

Industry‑specific trends

- Technology startups are gravitating toward convertible notes and venture debt, but still rely on SBA 7(a) loans for early‑stage capital.

- Manufacturing firms are using equipment financing to modernize production lines, taking advantage of tax‑credit incentives announced in the 2025 Inflation Reduction Act.

- Retail and hospitality sectors favor working capital loans to manage inventory turnover and seasonal payroll spikes.

How to Determine the Right Loan Type for Your Business

Choosing the right financing solution begins with a clear assessment of your cash‑flow needs, risk tolerance, and growth timeline. Follow these steps:

1. Map Your Funding Gap

Identify the exact amount you need and the purpose (e.g., $150,000 for equipment, $80,000 for inventory). Use a simple spreadsheet to project monthly revenue, expenses, and the net shortfall over the next 12‑18 months.

2. Evaluate Collateral Availability

If you own real estate, vehicles, or high‑value equipment, a secured loan will likely yield a lower rate. If not, consider unsecured options, but be prepared for stricter credit‑score requirements (typically 680+ for conventional lenders).

3. Compare Interest Structures

Fixed‑rate loans provide stability, while variable‑rate loans can be cheaper when the Federal Reserve lowers rates. For short‑term cash needs, a line of credit with a floating rate might be more flexible.

4. Check Eligibility for Government Programs

The SBA’s 7(a) and CDC/504 programs still dominate the low‑cost financing space. In 2025 the SBA approved 150,000 new loans, with an average size of $350,000. Eligibility typically requires a credit score above 640, less than 20 % debt‑to‑EBITDA, and at least two years of operating history.

5. Run the Numbers

Calculate the annual percentage rate (APR) and total cost of borrowing, including origination fees, prepayment penalties, and any required insurance. Use an online loan calculator or the spreadsheet model below:

- Loan amount: $200,000

- Term: 5 years

- Interest rate: 5.2 % (fixed)

- Monthly payment: $3,822

- Total interest paid: $29,320

Practical Steps to Secure a Business Loan

Once you’ve pinpointed the loan type, the application process is relatively uniform across banks, credit unions, and online lenders. Follow this checklist to improve approval odds:

Prepare Core Documentation

- Business plan with detailed financial projections (12‑month cash‑flow forecast).

- Recent tax returns (personal and business) for the past two years.

- Balance sheet, profit‑and‑loss statement, and bank statements (last three months).

- Collateral documentation (property deeds, equipment appraisals).

- Personal and business credit reports (obtain free copies from Experian).

Choose the Right Lender

Traditional banks still offer the best rates for well‑established firms, but fintech platforms like Kabbage and OnDeck can close deals in 24‑48 hours for smaller amounts. Consider the following criteria:

- Average approval time.

- Transparency of fees.

- Customer service ratings (check the Better Business Bureau).

- Availability of flexible repayment options.

Submit and Follow Up

After submission, lenders may request additional information—be ready to provide updated bank statements or a revised cash‑flow forecast. A prompt response can shave days off the underwriting timeline.

Common Mistakes to Avoid

Even seasoned entrepreneurs fall into traps that can inflate costs or cause loan denial. Watch out for these pitfalls:

- Over‑borrowing – Asking for more than you need leads to unnecessary interest expense.

- Ignoring the APR – Focusing solely on the nominal rate ignores fees that can raise the true cost.

- Poor Credit Management – Late payments on existing debt signal risk to lenders.

- Insufficient Collateral Documentation – Unclear ownership or valuation can delay approval.

- Choosing the Wrong Loan Term – Short terms increase monthly payments, while overly long terms raise total interest paid.

Case Study: A Midwest Manufacturing Firm’s Turnaround

In early 2025, a family‑owned metal‑fabrication shop in Ohio faced a cash‑flow crunch after a delayed contract. The owners applied for a $250,000 SBA 7(a) loan, using their factory building as collateral. By mapping a precise funding gap and presenting a revised three‑year revenue forecast, they secured the loan within 21 days. The infusion allowed them to purchase a new CNC machine, which boosted production capacity by 30 % and lifted annual revenue from $1.2 M to $1.6 M by Q4 2026. The case illustrates how aligning loan type with strategic objectives can generate measurable ROI.

Frequently Asked Questions

What is the difference between a term loan and a line of credit?

A term loan provides a lump‑sum amount repaid over a fixed schedule, while a line of credit offers revolving access to funds up to a limit, with interest only on the amount drawn.

Can startups qualify for an SBA loan?

Yes, if the startup has at least two years of operating history, a solid business plan, and a personal credit score above 640. The SBA also offers the Microloan program for amounts up to $50,000.

Are there any hidden fees I should watch for?

Common hidden costs include loan‑origination fees (1‑3 % of the principal), underwriting fees, and prepayment penalties. Always ask the lender for a full fee schedule before signing.

How does a working capital loan differ from an unsecured business loan?

Working capital loans are typically short‑term (6‑12 months) and may be secured by accounts receivable, whereas unsecured loans have longer terms but higher interest rates due to the lack of collateral.

What impact does a business loan have on my credit score?

Timely payments improve your business credit profile, while missed payments can lower both personal and business scores, affecting future financing options.

Future Outlook: What to Expect in 2027 and Beyond

Analysts at McKinsey & Company predict that digital underwriting platforms will dominate loan origination, cutting approval times to under 24 hours for qualified borrowers. Additionally, the Federal Reserve’s projected 2027 rate stability suggests that average loan rates could dip below 5 % for secured term loans, making borrowing even more attractive for growth‑oriented businesses.

Bottom Line

A well‑structured business loan can be the catalyst that transforms a modest operation into a market leader. By accurately assessing your funding gap, selecting the appropriate loan type—whether it’s an SBA‑guaranteed term loan, a working capital line of credit, or an equipment lease—and meticulously preparing your documentation, you position your company for approval and sustainable growth. Stay vigilant about costs, avoid common missteps, and keep an eye on emerging fintech solutions that promise faster, more transparent financing.

Ready to start? Review our step‑by‑step loan application checklist and take the first concrete step toward financing your next growth phase.

—

**Metadata**

– – – –